Discharge Of Indebtedness Income

Discharge Of Indebtedness Income - However, there are some instances. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts.

This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. However, there are some instances.

This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. However, there are some instances.

Statement Of From Discharge Of Indebtedness Worksheet

This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the..

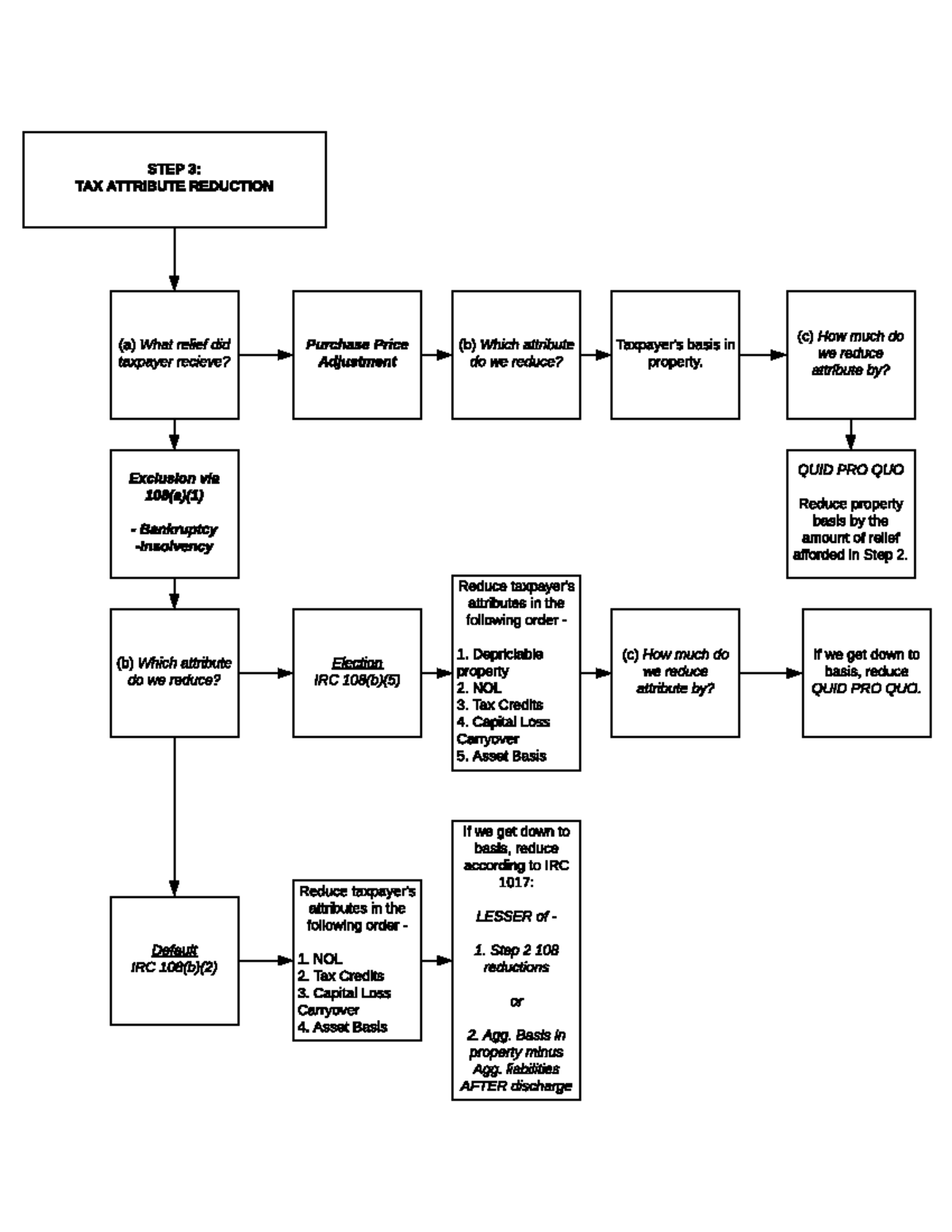

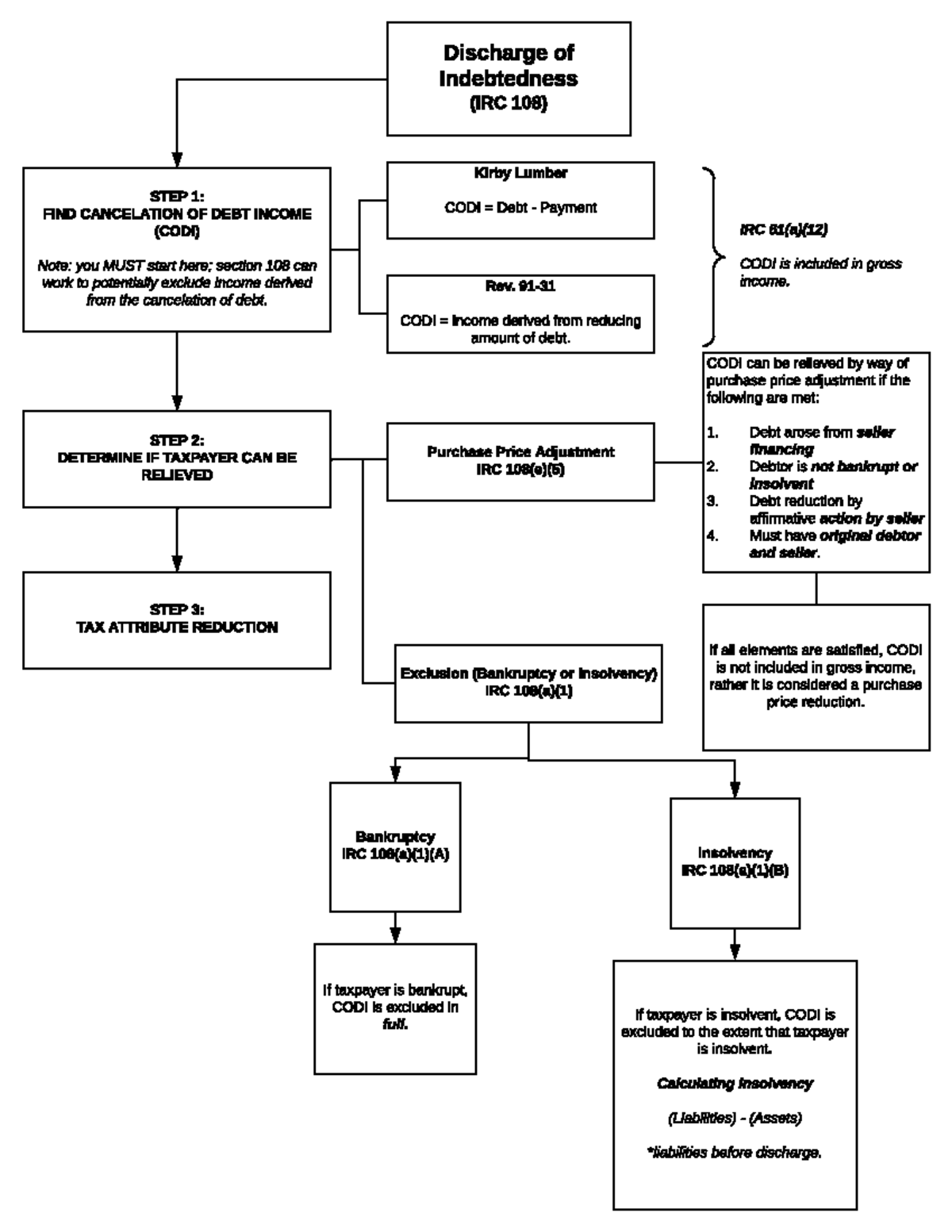

Discharge of Indebtedness Chart 2 STEP 3 TAX ATTRIBUTE REDUCTION

This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. However, there are some instances. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. To show that all or part of your canceled debt is excluded from.

Discharge of Indebtedness and Student Loan Ambler

However, there are some instances. This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. Gross income does not include any amount which (but for this subsection) would be includible in gross.

SOLVEDDetermine the amount of that must be recognized in each

A discharge of debt income occurs when a debt is forgiven by the person who lend the money. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. However, there are some instances. This section explains how to exclude or reduce gross income and tax attributes due.

General Rules of IRC Section 108 From Discharge Of Indebtedness

A discharge of debt income occurs when a debt is forgiven by the person who lend the money. This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach.

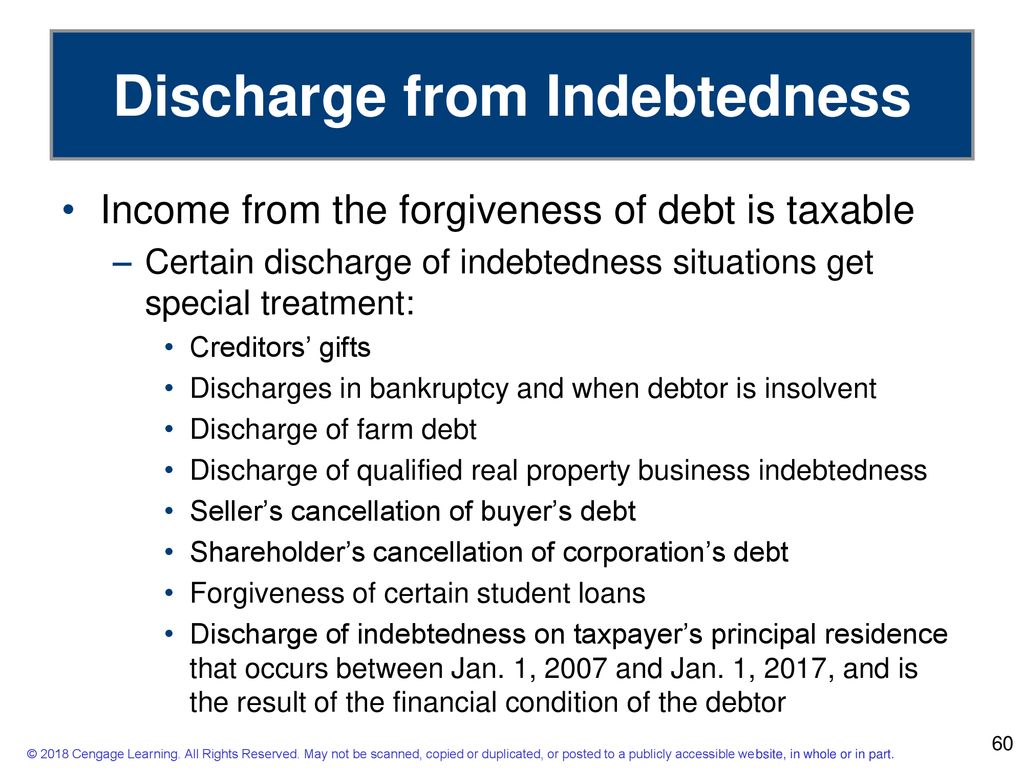

Washington & Lee University School of Law Tax Clinic ppt download

To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. However, there are some instances. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. Gross income does not include any amount which (but for this subsection) would be.

IRS Form 982 Instructions Discharge of Indebtedness

However, there are some instances. This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. Gross income does not include any amount which (but for this subsection).

Gross Exclusions ppt download

A discharge of debt income occurs when a debt is forgiven by the person who lend the money. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts..

Discharge of Indebtedness Chart 1 Discharge of Indebtedness (IRC

Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. However, there are some instances. This section explains how to exclude or reduce gross income.

IRS Form 982 Instructions Discharge of Indebtedness

This section explains how to exclude or reduce gross income and tax attributes due to the discharge of certain debts. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form. However, there are some instances. Gross income does not include any amount which (but for this subsection).

This Section Explains How To Exclude Or Reduce Gross Income And Tax Attributes Due To The Discharge Of Certain Debts.

However, there are some instances. A discharge of debt income occurs when a debt is forgiven by the person who lend the money. Gross income does not include any amount which (but for this subsection) would be includible in gross income by reason of the. To show that all or part of your canceled debt is excluded from income because it is qualified principal residence indebtedness, attach form.